Mar 01, 2019

As I made my Texas World Tour last year as president-elect, visiting all of our 18 chapters and sections, I…

There is a myth about homeownership — in America, and in many other societies. And myths can be costly. Homeownership is often characterized as a safe investment with a high return — as a hedge, a security blanket. Renting, on the other hand, is seen to be “throwing your money away,” and, whether or not as a result, numerous government programs encourage homeownership across the economic spectrum.

Qualitative assumptions that are hard to test are the ones that usually become legend, and the legend that homeownership is a valuable and cheap form of insurance against many housing risks is a case in point: Even careful academic research typically yields ambiguous results. Insurance policies spelling out coverage in the event of injury, illness, or natural disaster take a relatively concrete approach to specific risk; both the costs and the extent of the coverage are (relatively) clear. Social scientists can use the markets for these policies to understand how we feel about the underlying risks. However, the risks of renting and the “coverage” provided by owning a home are less clear and anyway not easy to observe or measure: There is no stated policy premium; there is no explicit coverage.

Homeownership is not unique in this regard; many types of “insurance” that we rely upon are implicit and in-kind, such as when a neighbor offers to look after our kids during an emergency (reminding us of the value of having neighbors). Though such “insurance” is hard to define, it is important in our lives and to our psyches: Believing we can rely on our neighbors when we are in trouble certainly gives us peace of mind.

This is all well and good, but normally, in-kind insurance does not have far-reaching implications for the world economy. Whether or not people are friendly with their neighbors has an impact only on such cottage industries as the afternoon tea party and the lemonade stand. Homeownership, on the other hand, is intricately connected with the transportation, construction, automobile, and finance industries (to name just a few). Its benefits have been elevated from the status of hearsay to ever-present fact: The “American Dream” has very real impacts on our waking lives.

PHOTOS BY LEONID FURMANSKY

We as a society, fueled by pop culture and folk wisdom, often consider homeownership to be a virtual panacea: a bulwark against the rising cost of living, one that provides protection from predatory landlords at little or no pecuniary cost. Our home is an intrinsic part of our identity, giving us and our families a sense of place and a haven for our memories and memorials. Homeownership, we may suppose, is our insurance against the forces that try to come between us and our roots.

Owning a home does provide some insurance, but this insurance doesn’t come for free. Houses, like cars, begin to depreciate the minute the papers are signed. The land on which the house sits might appreciate, but the structure does not. At best, you are buying insurance against the cost of the land going up. In many areas (including a lot of Texas), where most of the cost of housing is associated with the houses themselves and not the land, your housing purchase actually nets you very little in terms of security.

Nevertheless, it can be argued that owning a home is a good deal. Indeed, the fact that mortgage interest is tax deductible is a welcome subsidy to those that take the deduction. Since research shows that most of this subsidy’s benefit goes to relatively well-off households, perhaps more relevant to middle income families and poorer homeowners are the mortgage subsidies that are associated with government guarantees given to Freddie Mac and Fannie Mae. How much of either of these subsidies actually goes to new homeowners instead of merely inflating prices depends a lot on how much new supply is being added to their market.

Financing a home purchase has become much easier over the years: A century ago, the typical mortgage came with a three-to-five-year balloon payment and allowed no more than a 50 percent loan-to-value ratio. Now, you can often borrow in excess of 90 percent of the home’s value by taking out several mortgages at once. And you can borrow the money for 30 years at a fixed rate, which takes away the risk of a balloon payment down the line. Dollar for dollar, these modern lending practices have made financing homeownership safer for households and for banks, and yet they have also raised the price of housing in many areas, effectively expanding America into areas with cheaper land – the suburbs.

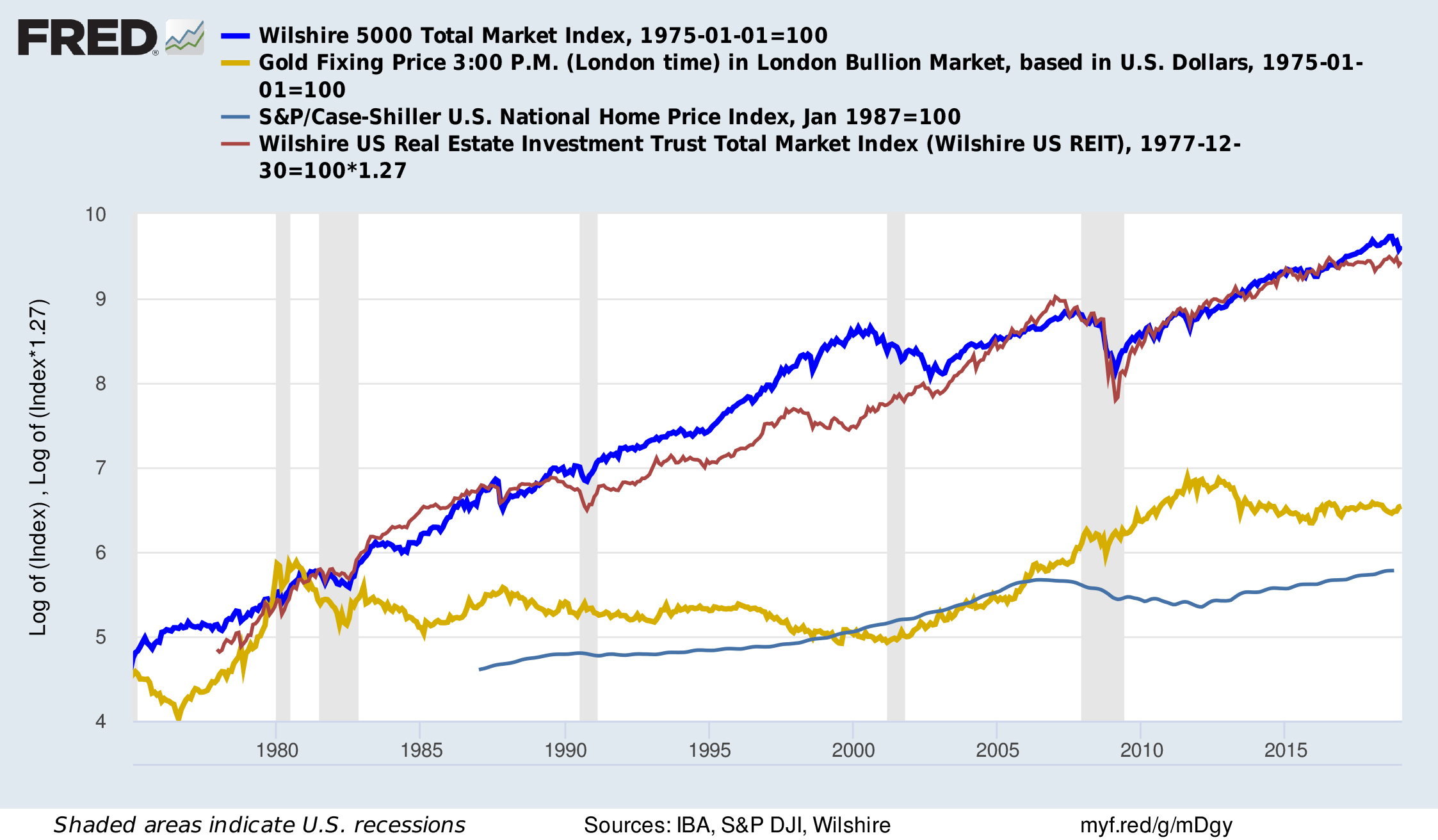

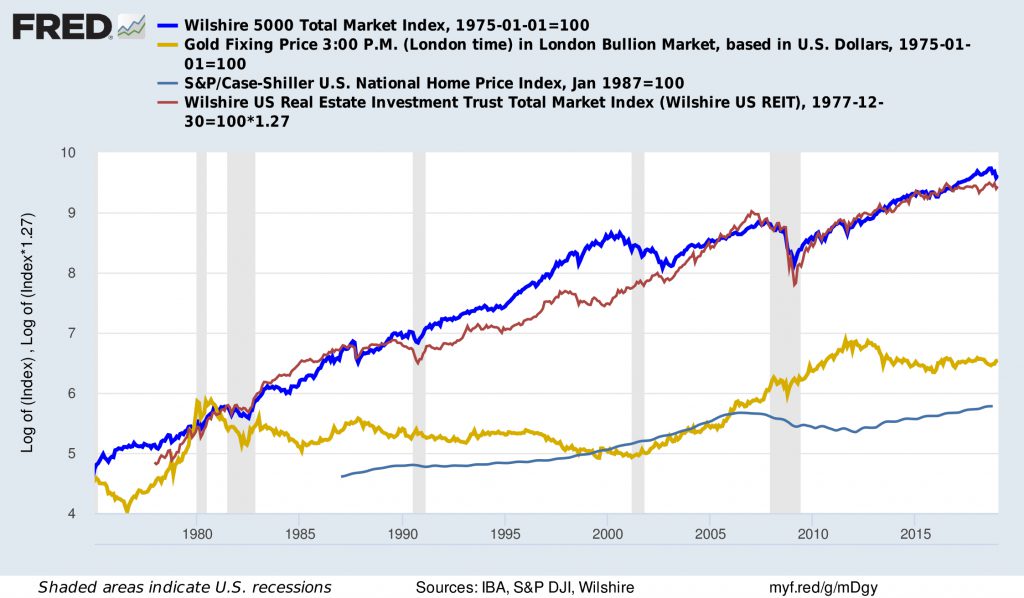

With a downpayment of $100,00, you can typically get a loan for a million-dollar house, these days, but increased leverage and long maturities expose households to other risks. For instance, a 30-year mortgage accrues equity very slowly: At an interest rate of six percent, a buyer who puts 10 percent down to buy has built up only 16 percent in equity at the end of five years. This means that house prices need only fall a few percentage points to wipe out any wealth the homeowner thought he had accumulated. According to the Standard and Poor’s Case-Shiller index, the average national house price fell around 25 percent between 2006 and 2012. More typically, house prices grow far more slowly than do many stock indices. Only leverage and its commensurate risk make investing in housing an equivalent return proposition to a diversified financial portfolio (and that is without figuring in some of the tax advantages of various retirement savings plans). Moreover, once the mortgage is paid off, you may be “free and clear,” but you also now have a lot of wealth sunk into something that, on average, grows far more slowly than a plain vanilla stock portfolio would. Factor in the customary transaction costs of buying, selling, and financing a house, and owning a home is anything but a risk-free or cheap way to build wealth.

Meanwhile, rents at the local level aren’t very volatile. Rents grew during the housing boom, but not by nearly as much as house prices did. They fell during the bust, but not by nearly as much as they had previously grown. Rents move much more reliably in tandem with local wages than do local house prices. Local rents tend to be driven by local housing demand, of which local household income is an important part. Rents are relatively stable, because local average wages are relatively stable. House prices, on the other hand, really reflect three, more psychological concerns: (1) the degree to which the homeowner expects his purchase to protect him from future costs, including future costs of renting instead; (2) how patient the homeowner and the market are (a dollar now is worth more than a dollar will be in the future); and (3) the willingness of the homeowner and the market to bear risk. This is quite a discrepancy: Our expectations for the future and desire to bear risk are, like dreams, rather less tethered to our immediate realities than our current paychecks are.

So, if you’re a typical worker earning a typical local income, it turns out you already have a good insurance policy (or, in finance parlance, a good “hedge”) against rising rents: your rental bill is only growing about as fast as your income. However, the typical renter in many U.S. cities is not the typical worker. Low-skilled workers’ and public sector workers’ incomes often do not keep pace with local average wages (e.g., the public school teacher in Manhattan, the janitor in Silicon Valley), and so these people face the risk of being priced out of their housing market. Of course, this is the very swath of America — and of nearly every booming metropolis in every other developed country — that is usually not able to accrue wealth fast enough to buy a house. For them, homeownership is as elusive as a dream. So the very households for whom renting is most financially risky are also the ones who cannot afford the insurance policy of homeownership.

Various forms of rent control could offer security to these households, at the cost of extreme distortions to the market. Rent control is generally disastrous, and I am not aware of a rent policy deployed at scale whose medicine wasn’t worse than the sickness it was supposedly curing. Many (but by no means all) of the social costs of rent control fall on “outsiders” — households that are unable to enter the controlled market. This means that, ironically like many of the mooted benefits of homeownership, many of the costs of rent control are shadowy and prone to debate. Like with many price controls, there are better ways of achieving the same policy ends.

Of course, renting also poses nonfinancial risks: the risk of being displaced by the landlord’s cousin; the risk of having a “slum” landlord that under-maintains. So does owning, though: While a renter can relatively quickly abandon a house that has problems (termites, mold, a bad neighbor), a homeowner typically has to stick it out, unless he or she defaults on the mortgage.

As with the financial hedge, the nonfinancial risks of renting are often most acute for the types of renters that can least afford owning. If you were to rent a nice $1 million home in a suburban area, the landlord has an incentive to help ensure the house is well-maintained and thus holds its value. Such landlords often value good tenants in return and treat them well; a bad tenant can be a nightmare for a landlord. In these cases, landlords are less likely to “see what the market will bear” by raising rents and forcing out a current tenant.

On the other hand, if you are renting an old, cheap three-bedroom bungalow in a high value area of a city, you’re really mainly renting the land from the landlord. If a new buyer is just going to tear down the house, the current structure itself has little value in the market and thus to the landlord. The incentive to maintain it is low and the chance it falls into some kind of disrepair, high. Of course, again, the tenants of this older house are exactly the ones that are likely not to be able to afford to buy an anywhere-near-comparable house in the neighborhood (to say nothing of a newer house).

Americans are less mobile than they used to be. Data show that they move to new places less frequently than they did a generation ago. Data also show that Americans are more geographically segregated by income, wealth, and politics than their parents were. Younger Americans may be able to carry their online social network wherever they may live, but where they live is increasingly stratified and homogeneous. And, as America recovers from the housing bust, it continues to suburbanize: The thirst for a place for one’s own gives rise to more bedroom communities, and, therefore, homeownership continues.

What’s not clear from these trends is how our sense of place may be evolving. Our horizons are expanding, but we still want to know who our kids are playing with. Homeownership is sold as the ultimate insurance — even if it comes at some cost — against losing your neighbors, your parish, that great school for your kids — and so many other forms of local social capital. A home is a shield from prying eyes, too: Nobody notices if you forgo a vacation in tough times, but move to a smaller house down the block and everyone in your neighborhood might be clued in to your financial straits.

Since the housing boom and bust, homeownership as a public policy goal is increasingly being questioned. Function often follows form, though, so unless we develop housing and design our communities for renting, homeownership will still be a personal goal for many households. What interests me going forward is understanding in what ways other than homeownership various communities can help ameliorate housing fears. How can we better plan our communities and design and develop our buildings and streets (and not just our online networks) in order to provide better and lower-cost implicit social safety nets for our families?

Jonathan Halket is an assistant professor at the Mays Business School at Texas A&M University.