Nov 20, 2017

There is a small crack in the flashing around one of the pipe vents that protrudes from my house’s metal…

In the years leading up to the last Great Recession, a funny thing happened. A thing unprecedented in the 20,000 years in which humans have been building buildings. This little flip occurred without much fanfare. It would forever change the landscape of architecture, the architecture of landscape, the form of our cities, and, not insignificantly, our employment possibilities.

In a way, the Little Flip caused the Great Recession. It will cause the next one too. It festers apolitically at the heart of #russiagate. It’s probably touched every architect you know in some way.

I’ll explain. But first, a little history:

For all of human history, humans built useful buildings because they needed them. If they needed shelter, they built a house. If they needed to house some animals, they built a barn. There are, of course, varying ways to understand “need.” Did the pharaohs “need” to build the pyramids as personal mausoleums? It seems excessive. But I’m sure if you asked them they would be quite clear about the fact that they needed a massive burial chamber so that they could be buried with all their stuff. I am certain that the ultra-wealthy were then allowed to be eccentric, same as they are now.

This system persisted until the mid-1930s, when the modern mortgage system came into being. Prior to that, lending was very sparse and very expensive, so if you built something, it meant you probably already had the money, or most of it. It also meant that whatever you were building was very, very necessary. For perspective, the typical mortgage in the 1920s would require a 50% down payment, have a term of five years, and interest rates north of 20 percent. It was like buying a house on a really terrible credit card.

At some point, the finance community saw the coming pitchforks and decided that it was probably okay to lend non-wealthy people money, so long as those loans were secured by the government. Washington thought that growing prosperity was a good idea, so kicked in with the full faith and credit of the U.S. Government. This led to all sorts of cool new toys, like Fannie Mae, and Freddie Mac, and the U.S. Small Business Administration, and the full canon of our national lending laws.

In the sum of all these changes, we enjoyed a progressive shift: Instead of worrying about the building you needed today, you could worry about the building you needed tomorrow. And thus, modern real estate development was born. One could go into a bank and claim that five years from now, or 10 years from now, there would be an increased need for housing, or grocery stores, or whatever. You would need to back up your claim with research or demographic data, but assuming that that was convincing, you could get a loan (mortgage). Such a loan would be granted based on the anticipated future needs of a community, and a developer could begin (obviously, with an architect). Occasionally, people would misjudge the market, but the nature of Keynesian capitalism kept everyone fairly honest. The postwar boom is the convincing evidence of the efficacy of this system: lots of work for developers, contractors, engineers, and architects, and cities tended to get the buildings they needed (or would need).

The financial deregulation of the 1980s allowed an entirely new form of capital to arise out of our built environment through the miracle of securitization. The Great Recession brought into view a particular phenomenon: Once one had built a building, one needed to sell it.

The buyer would need a mortgage, and mortgages could subsequently be bundled into securities that traded extremely well. The desire for these securities was so strong that it altered our entire culture of lending and home-buying. Banks got in the business of pushing sub-prime loans to people who couldn’t afford them, and we all know how that turned out.

While subsequent financial reform eliminated the problem of sub-prime residential mortgages, the wider phenomenon of asset-backed securities is larger than ever. Commercial mortgage-backed securities (CMBS) operate in essentially the same fashion. They bundle together commercial mortgages to create securities that can then be sold to investors. In fact, just about anything can now be “securitized” and resold. Same as the mortgage crisis, the securities eventually prove more desirable than the stuff they’re made of. So they trade better.

How’s that work? Historically, the number of buildings we produce has to do with need and utility and, ultimately, demographics. As populations grow, move, or concentrate in a particular area, we need more buildings, or newer buildings. Since we can’t have a mortgage without a building, one would think that the market for securities is indirectly limited by demographics. We can’t build a building if there’s no market to support its use, right? That is, assuming the housing/commercial market is functioning properly.

Since the Little Flip, evidence is all around us that the “market” is failing to address the needs of the market. The issue of “affordable” housing has now become even a middle class discussion. While we seem to have a glut of luxury properties that Americans are unable to afford, last year, California only built one new home for every 3.78 new residents. In pure economic terms, the “market” is over-supplying luxury homes and under-supplying everything else.

A quick drive through any American city will see multiple new condo tomorrows being erected, absent the schools, parks, grocery stores, and other dimensions of community. What changed? The Little Flip. In the simplest terms: Mortgages became more desirable than buildings. Before, in order to have a building, one needed a mortgage. Now, in order to have a mortgage, one needs a building. And so we build.

These buildings may be designed under the auspices of “luxury housing” or “commercial office space,” but fundamentally they’re not generated for that purpose.

Rich people need places to live too, and personally I’ve never objected to the fact that some architects will serve that portion of the market; buildings are expensive, and architects need fees. We should believe, however, that forces of the market would act to employ architects across the socioeconomic spectrum. There is a market for middle-class housing, same as there is a market for the housing of rich people. The problem here is that neither of those markets is being served. What is being served is the market for investment securities. Buildings are just a means to an end.

In order to motivate the building of a building, one no longer needs to need a building, or even justify the future need for a building. The endless need for more investment securities trumps both.

The profession of architecture needs to consider its role in all of this. As stewards and champions of the built environment, we must consider that space has always been a type of capital. In recent times, it has become two forms of capital: Two forms of capital that we had previously believed were inextricably linked have now become separated.

Real estate has always been considered an asset. Architects help create the value of that asset through the thoughtfulness and the appropriateness of their designs. But fundamentally, the value of that asset is tied to a building’s usefulness — meaning, if people want to use it, it retains (and grows) its value. But what if there’s no market for use? What if it’s not valuable as housing, or office space, or retail, because no market exists for any of those things? What if there’s no possible use for a building, other than to exist on the balance sheet of a foreign corporation? Certainly we can still get paid to design these sorts of buildings, but there are two reasons we shouldn’t do it.

The moral imperative: For all the crowing about “health, safety, and public welfare,” architects need to eschew any design process that will ultimately be antagonistic to those purposes. Any building designed to be uninhabited degrades neighborhoods’ public safety, culture, and social welfare.

For any architect who needs a “business” reason to get out of this business, here’s one: It’s completely unsustainable. When a market for buildings is based on population, or human need, or social need, it’s sustainable as long as the species continues to grow. As people reproduce and get wealthier, we need buildings. Buildings need designing, and so architects have work.

Money tends to go where it’s optimized. So money flows into this market because the other options are worse. If the yield in the international bond market rises, for instance, the international investing community will drive its funds toward bonds, instead of real estate, leaving our cities with forests of hulking, unfinished, ultra-luxury towers, occupied by no one. The possibility should seem familiar to any veteran of the 2008 crash; Forbes magazine went so far as to call it “The Rich Man’s Sub-Prime.”

When we design cities for people, the cities fill themselves up with people. Rich people, poor people, middle class people. The educated, the ignorant, the selfish, and the altruistic. This diversity eventually leads to a shared experience that everyone is invested in. It promotes conflict, but also reconciliation. That is how cities grow, and prosper.

When we design cities exclusively for investment purposes, they die slowly. The various forms of “capital” that buildings can produce eventually fall away. What’s left is a purely monetary form of capital only really relevant to a tiny clique of wealthy investors — the ones who don’t live there.

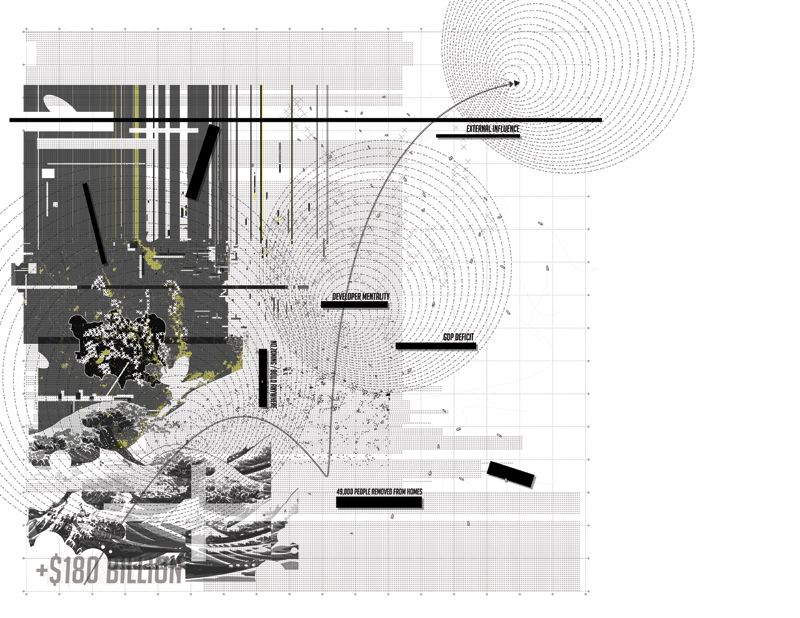

The recent destruction in Houston and Miami points to an even more desperate consequence: Cities of capital won’t protect themselves. Losses are insured — often for more than they’re worth. The destruction of a $3 million condo by a Harvey or an Irma isn’t necessarily considered a loss, if it’s not your city. You may even turn a profit.

The Little Flip has already had profound consequences for our cities and our future, all the while allowing architects to continue working and the Architecture Billings Index to keep rising. But a devil’s bargain always comes to an end, and never a good one. We will see further housing shortages, further disasters, and the eventual collapse of the architectural economy, along with the firm closures and layoffs we have just begun to forget. For our economic health, and the moral soul of architecture, we must resist.

Eric J. Cesal is a designer, writer, and noted post-disaster expert, having led on-the-ground reconstruction programs after the Haiti earthquake, the Great East Japan Tsunami, and Superstorm Sandy. Cesal’s formal training is as an architect, with international development, economics and foreign policy among his areas of expertise. He works for the Curry Stone Foundation as Director of Special Projects and is a Visiting Lecturer on Disaster and Resilience at UC Berkeley.